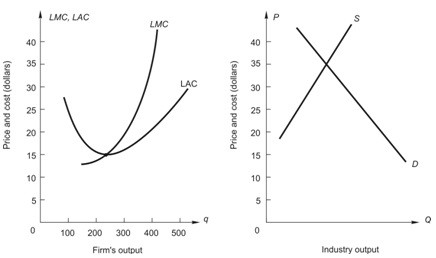

Below, the graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry. The graph on the right shows demand and long-run supply for an increasing-cost industry. How much profit will the firm earn?

How much profit will the firm earn?

A. $3,100

B. $2,600

C. $3,750

D. $6,000

E. zero

Answer: D

You might also like to view...

If marginal propensity to save equals 0.50, then the marginal propensity to consume is:

A) 1.25. B) 0.50. C) 0.70. D) 1.00.

A decrease in supply will cause an increase in price, which will cause a decrease in quantity demanded

a. True b. False Indicate whether the statement is true or false

Which of the following statements is correct?

A. Total utility is the change in marginal utility as quantity consumed increases. B. Marginal utility is the sum of total utility. C. Total utility is the product of multiplying price times marginal utility. D. Total utility is the sum of marginal utilities.

Oligopolists compete on quality but not price.

Answer the following statement true (T) or false (F)