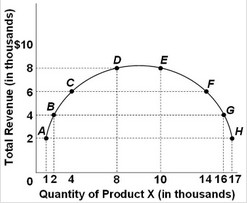

Use the following graph of total revenues to answer the question below.  If the quantity of product X demanded decreases from 16,000 to 10,000 units, then it suggests that the price of X was

If the quantity of product X demanded decreases from 16,000 to 10,000 units, then it suggests that the price of X was

A. reduced and the demand is elastic.

B. increased and the demand is elastic.

C. increased and the demand is inelastic.

D. reduced and the demand is inelastic.

Answer: C

You might also like to view...

A ________ monopoly sells different units of its good or service for ________

A) price-discriminating; different prices B) price-discriminating; the same price C) single-price; the same price D) single-price; different prices E) Both Answers A and C are correct.

As the MPC gets close to 1, the value of the multiplier approaches

a. 0. b. 1. c. infinity. d. None of the above is correct.

Writing in the New York Times on the technology boom of the late 1990s, Michael Lewis argues, "The sad truth, for investors, seems to be that most of the benefits of new technologies are passed right through to consumers free of charge." What does Lewis

means by the benefits of new technology being "passed right through to consumers free of charge"? A) Firms in perfect competition are price takers. Since they cannot influence price, they cannot dictate who benefits from new technologies, even if the benefits of new technology are being "passed right through to consumers free of charge." B) In perfect competition, price equals marginal cost of production. In this sense, consumers receive the new technology "free of charge." C) In the long run, price equals the lowest possible average cost of production. In this sense, consumers receive the new technology "free of charge." D) In perfect competition, consumers place a value on the good equal to its marginal cost of production and since they are willing to pay the marginal valuation of the good, they are essentially receiving the new technology "free of charge."

Banks with excellent credit can borrow ________ from the Federal Reserve.

A. an unlimited amount B. $1,000,000 per year C. only an amount equal to their deposits D. $1,000,000 per day