Refer to the information provided in Table 24.4 below to answer the question(s) that follow.

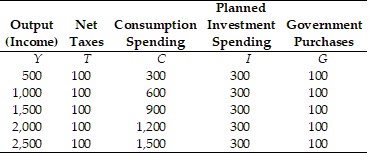

Table 24.4 Refer to Table 24.4. At an output level of $1,500 billion, there is an unplanned inventory

Refer to Table 24.4. At an output level of $1,500 billion, there is an unplanned inventory

A. change of $0.

B. increase of $100 billion.

C. increase of $200 billion.

D. decrease of $200 billion.

Answer: C

You might also like to view...

In the United States during the Great Depression, tariffs were ________ than they were following World War II, and ________ than they are today

A) higher; higher B) higher; lower C) lower; lower D) lower; higher

Which of the following is true in long-run equilibrium for both perfect competition and monopolistic competition?

a. Accounting profit is zero. b. Marginal cost equals price. c. Long-run average cost is at a minimum. d. Economic profit is zero.

When economists say an individual displays economizing behavior, they simply mean that she is

a. making a lot of money. b. buying only those products that are cheap and of low quality. c. learning how to run a business more effectively. d. seeking the lowest cost method to accomplish her objectives.

How is the long-term result of entry and exit in a perfectly competitive market different from that in a monopolistically competitive market?