If marginal cost is constant, what happens to a market if it alters from perfect competition to monopoly without any change in the position of the market demand curve or any variation in costs?

A. Consumer surplus increases, producer surplus decreases and a deadweight loss is created.

B. Consumer surplus increases, producer surplus increases and a deadweight loss is created.

C. Consumer surplus decreases, producer surplus decreases and a deadweight loss is created.

D. Consumer surplus decreases, producer surplus increases and a deadweight loss is created.

Answer: D

You might also like to view...

If the Fed increases the quantity of money, in the short run the ________ and in the long run the ________

A) nominal interest rate falls; the price level falls B) nominal interest rate falls; the price level rises C) price level rises; the nominal interest rate falls D) nominal interest rate rises; the price level falls E) nominal interest rate rises; the price level rises

Real income is ________

A) equal to money income minus taxes B) equal to the income earned legally C) equal to money income plus benefits minus taxes D) the maximum amount of goods and services that a household can afford

Suppose your instructor gave hats with your school's logo to half of your economics classmates. She then asked these students to value the hats, and the average response was $9 per hat

Under the endowment effect, we should expect that the average value assigned by the economics students who did NOT receive the hats to be: A) higher. B) lower. C) the same. D) We cannot answer this question without knowing more about the risk preferences of the students.

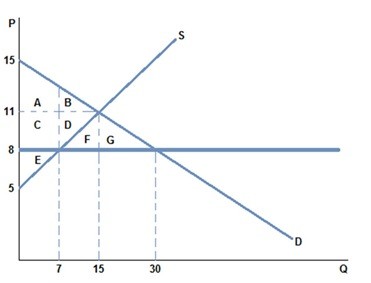

If a price ceiling of $8 were placed in the market in the graph shown:

If a price ceiling of $8 were placed in the market in the graph shown:

A. an excess supply of 23 would occur. B. an excess supply of 15 would occur. C. an excess supply of 7 would occur. D. None of these is true.