If the quantity you buy of a good increases when your income increases, the good is clearly a(n)

a. essential good

b. inferior good

c. substitute good

d. complementary good

e. normal good

E

You might also like to view...

At the point of maximum profit, marginal revenue equals

a. variable cost. b. fixed cost. c. average total cost. d. marginal cost.

The "Public Choice" school of economists argue that:

a. the invisible hand of the market is inefficient in allocating resources to their best uses. b. the government often does not take correct economic decisions as it is run by self-interested politicians. c. the government takes correct decisions as it is run by conscious and educated individuals. d. the market fails to maximize social efficiency. e. the government is a non-profit making organization which works to maximize social efficiency.

When competition is present and private ownership rights are clearly defined and securely enforced by the legal system, business firms will have a strong incentive to

A) innovate and develop better products and lower cost production methods. B) engage in wasteful activities that increase the cost of producing goods and services. C) use resources during the current period rather than conserving them for the future. D) spend time attempting to plunder (take) the resources of others.

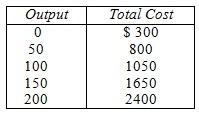

Based on the following table, what is total variable cost when 100 units of output are produced?

A. $105 B. $5 C. $10.50 D. $1050 E. none of the above