In Problem 5, in the long run, what is the market price and the quantity of paper produced? What is the number of firms in the market?

What will be an ideal response?

In the long run, the price equals the minimum average total cost, $10 a box. The number of firms in the long run is 750 . In the long run, as firms exit the industry, the price rises. In the long-run equilibrium the price will equal the minimum average total cost. When output is 400 boxes a week, marginal cost equals average total cost and average total cost is a minimum at $10 a box. In the long run, the price is $10 a box. Each firm remaining in the industry produces 400 boxes a week. The quantity demanded at $10 a box is 300,000 boxes a week. The number of firms is 300,000 boxes divided by 400 boxes per firm, which is 750 firms. In the long run, the 750 firms together produce the equilibrium quantity of 300,000 boxes.

You might also like to view...

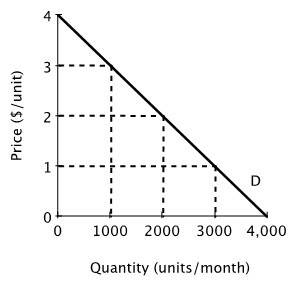

Quick Buck and Pushy Sales produce and sell identical products and face zero marginal and average cost. Below is the market demand curve for their product.  Suppose Quick Buck and Pushy Sales decide to collude and work together as a monopolist with each firm producing half the quantity demanded by the market at the monopoly price. If Quick Buck cheats by reducing its price to $1 while Pushy Sales continues to comply with the collusive agreement, then Quick Buck's economic profit will be ________.

Suppose Quick Buck and Pushy Sales decide to collude and work together as a monopolist with each firm producing half the quantity demanded by the market at the monopoly price. If Quick Buck cheats by reducing its price to $1 while Pushy Sales continues to comply with the collusive agreement, then Quick Buck's economic profit will be ________.

A. $3,000 B. $6,000 C. $4,000 D. $2,000

The life-cycle hypothesis was developed in the 1950s, primarily by the economist

A) Franco Modigliani. B) Robert Lucas. C) Walter Rostow. D) Nils Hellstrom.

The law of diminishing marginal utility explains why:

A. supply curves slope upward. B. demand curves slope downward. C. addicts can never get enough. D. people will only consume their favorite goods and not try new things.

When consumers spend and buy things regardless of their level of income, this is known as:

A. bad financial management. B. living the good life. C. autonomous consumption spending. D. using credit to its maximum.