As the number of firms in an industry increases, the residual demand curve becomes

A) more elastic.

B) less elastic.

C) larger.

D) vertical.

A

Economics

You might also like to view...

If an economy is growing at a rate of 2.5% per year, how long will it take the economy to double in size?

A) 60 years B) 43 years C) 36 years D) 28 years

Economics

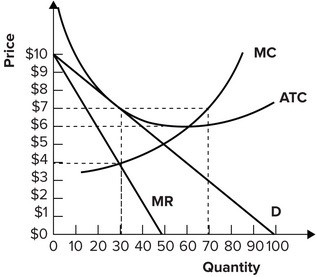

Refer to the graph shown. The equilibrium quantity for the monopolistically competitive firm represented is:

A. 70. B. 30. C. 50. D. 60.

Economics

Under perfect competition, price is equal to

A. marginal revenue. B. total revenue divided by output. C. average revenue. D. All of the choices are equal to price under perfect competition.

Economics

As economists use the word, investment refers only to an increase in capital.

Answer the following statement true (T) or false (F)

Economics