From the Industrial Revolution to the present, innovation has played a major role in the growth of output. What do the leading analysts of economic growth argue were some of the most significant innovations of this period?

Leading analysts of economic grow argue that some of the most significant innovations were electricity, use of radio waves to transmit sound, discovery of the new technique for refining iron, products such as the automobile, airplane, transistor, integrated circuit, and computer.

You might also like to view...

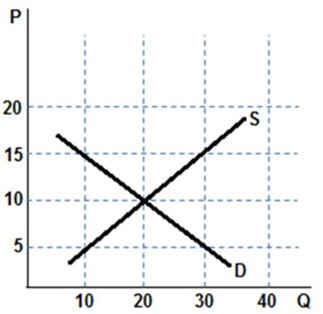

According to the graph shown, at a price of $5, there is a:

According to the graph shown, at a price of $5, there is a:

A. shortage of 10. B. shortage of 30. C. shortage of 20. D. surplus of 20.

Which of the following changes is most likely to happen when there is a decrease in the supply of money in a market that was initially in equilibrium?

a. The demand for money increases b. Planned investment spending increases c. Interest rate increases d. Aggregate expenditure increases e. The demand for money decreases

If you must make a choice about consuming two apples, three oranges, or one candy bar, the opportunity cost of the two apples is the candy bar plus the three oranges

a. True b. False Indicate whether the statement is true or false

The concept of relative poverty

A. leads to the concept of inequality. B. replaces the need for concepts of absolute poverty. C. is measured relative to the poverty line. D. is only relevant in low income countries.