Which is not true of a perfectly competitive market?

A. The typical industry demand curve is downward sloping.

B. If the long-run average total cost curve is horizontal in the relevant range of production, perfectly competitive firms can be various sizes in long-run equilibrium.

C. There is no incentive to innovate since economic profit is zero in the long-run.

D. At long-run equilibrium, economic profit is less than accounting profit.

Answer: C

You might also like to view...

Disinflation refers to

A) a rapid increase in the price level. B) a decrease in the price level. C) a reduction in the rate of inflation. D) an increase in the rate of inflation.

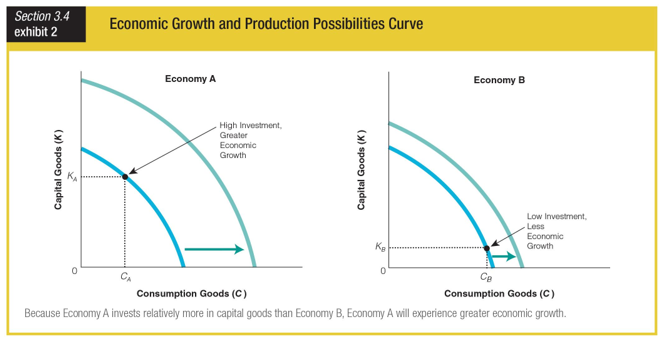

How did different levels of investment influence the production possibilities curves in this economic growth and production possibilities curve?

a. Economy A saw its curve contract inward.

b. Economy A saw its curve shift further outward than Economy B.

c. Economy B saw no change in its curve.

d. Economy B saw its curve shift from concave to a straight line.

The distinguishing characteristic of private goods is that

A) the principle of rival consumption does not apply to them. B) their use is exclusive to the people who purchase them. C) they can be sold but not rented. D) they can be sold or rented, but not borrowed.

For a monopolist, the marginal revenue gained when one more unit of output is sold is

A) the price at which the extra unit is sold minus the loss in revenue that results from cutting the price on units sold previously. B) equal to the price of the product. C) negative if price is above the midpoint of the demand curve. D) the average revenue created by the increased sales.