Suppose that initially a market is in equilibrium at a price of $10 and a quantity of 5000 units per day. Several months later, the market is in a new equilibrium at a price of $5 and a quantity of 5000 units per day. What happened in the market?

What will be an ideal response?

For price to fall, either demand had to decrease or supply had to increase, or both. If demand decreased while supply remained constant, the quantity would have decreased too, and if supply increased while demand remained constant, the quantity sold would have increased. Therefore, both demand decreased and supply increased in such a way that the quantity did not change.

You might also like to view...

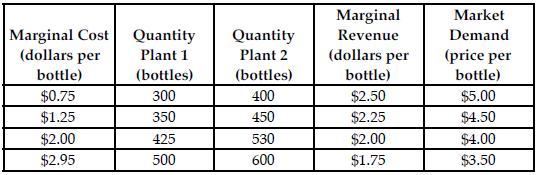

Refer to the table below. What is the profit-maximizing quantity for Just Juice to produce at Plant 1?

Just Juice produces whole fruit juice that it sells in single bottles. Just Juice is a multi-plant firm with market power. The above table summarizes the total marginal cost of production at various output levels in Just Juice's two plants with the corresponding marginal revenue (dollars per bottle) and market demand (price per bottle).

A) 350

B) 530

C) 500

D) 425

One characteristic of an efficient tax system is that it minimizes the costs associated with revenue collection

a. True b. False Indicate whether the statement is true or false

How does the method of increasing revenue differ when demand is price inelastic and price elastic? Explain.

What will be an ideal response?

Exhibit 2-11 Production possibilities curves In Exhibit 2-11, which of the following could have caused the production possibilities curve of an economy to shift from the one labeled A to the one labeled B?

In Exhibit 2-11, which of the following could have caused the production possibilities curve of an economy to shift from the one labeled A to the one labeled B?

A. A major natural disaster B. An increase in consumption goods production this year C. An advance in technology D. An increase in unemployment