Refer to the above table. Suppose the marginal revenue product of the 7th worker is $1100. This implies that

A) the price of the good is $1.

B) the price of the good is $8.

C) the price of the good is $20.

D) we cannot tell what the price of the good is without more information.

C

You might also like to view...

Total fixed cost is the sum of all

A) costs of the firm's fixed factors of production. B) costs associated with the production of goods. C) costs that rise as output increases. D) the marginal costs of the different factors of production.

When a firm decides to shut down in the short run, its losses are limited to its fixed costs

Indicate whether the statement is true or false

Games:

A. will always have several stable outcomes. B. are always zero sum. C. will always have a dominant strategy. D. None of the above are true.

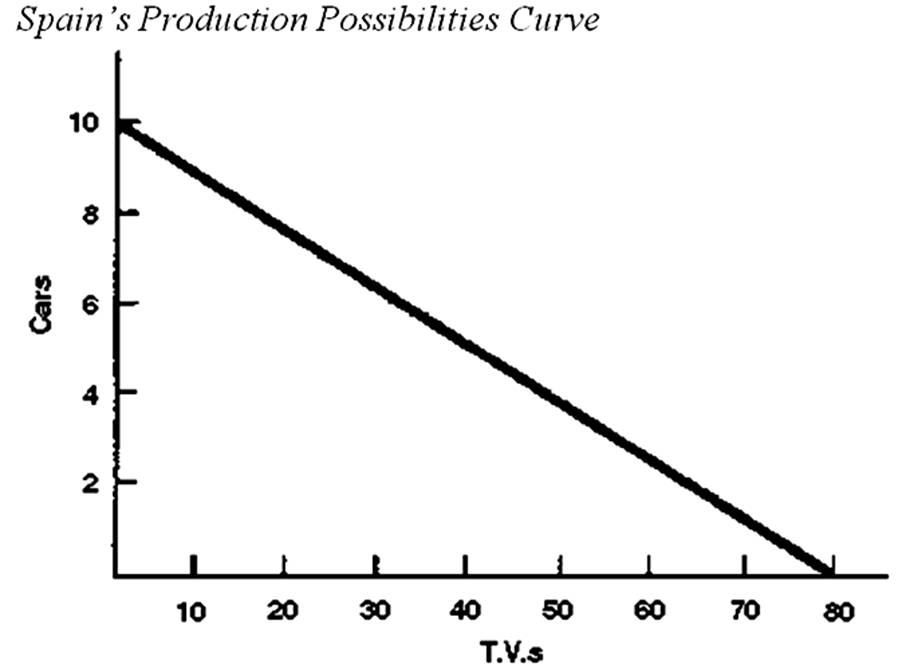

Assume that Spain will specialize in either cars or TVs. What is their opportunity cost of producing one car?