The equilibrium price is the price where quantity demanded is equal to supply

a. True

b. False

Indicate whether the statement is true or false

False

You might also like to view...

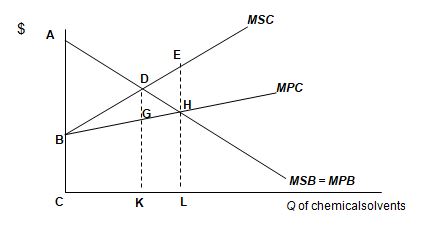

At QC, the maximum payment recreational users of the river would be willing to pay the producer for a unit change in output is

Consider the following graph of the market for chemical solvents, production of which damages a waterbody used for recreation.

a. DG b. DEH c. EH d. none of the above

The "Law of Diminishing Returns" states that

A) additional inputs will reduce output. B) additional inputs will decrease average productivity. C) the supply of inputs is becoming scarce. D) additional inputs will lead to less additional output.

The term inflation is used to describe a situation in which

a. the overall level of prices in the economy is increasing. b. incomes in the economy are increasing. c. stock-market prices are rising. d. the economy is growing rapidly.

By summing the dollar value of all market transactions in the economy we would:

a) determine the market value of all resources used in the production process. b) obtain a sum substantially larger than the GDP. c) determine value added for the economy. d) measure GDP.