We can draw demand curves for firms in perfectly competitive and monopolistically competitive industries, but not for oligopoly firms. The reason for this is

A) there are no barriers to entry in perfectly competitive and monopolistically competitive industries. There are high barriers to entry in oligopoly industries.

B) we can assume that the prices charged by perfectly competitive and monopolistically competitive firms have no impact on rival firms. For oligopoly this assumption is unrealistic.

C) that perfectly competitive and monopolistically competitive firms are price takers. Oligopoly firms are price makers.

D) perfectly competitive and monopolistically competitive firms sell standardized products. Oligopoly firms sell differentiated products.

Answer: B

You might also like to view...

Which of the following is a macroeconomic subject?

a. umbrellas produced by a firm b. wages earned by a firm producing umbrellas c. cost of producing military aircraft d. savings in the national economy e. profit earned by a firm producing military aircraft

For some economists, it is hard to refute the validity of the war-induced theory of business cycles because for World War I, World War II, and the Korean War, the war- induced expansion came

a. when the economy was in the upswing or peak phase of an already existing cycle b. when the economy was in the upswing or trough phase of an already existing cycle c. when the economy was in the downswing or trough phase of an already existing cycle d. when the war was already over, causing a downswing in an already existing cycle e. in the aftermath of each war

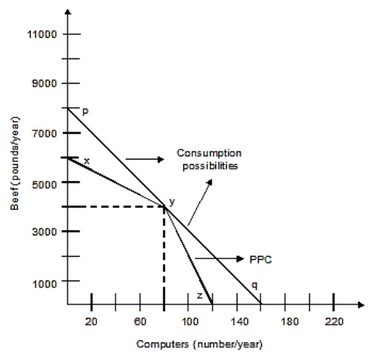

The following graph shows the production possibilities curve for the economy with only two members, Silvia and Art. Silvia can produce either 50 pounds of beef or 2 computers per week, and Art can produce 100 pounds of beef or 1 computer per week. Both of them work 40 weeks per year. Art's opportunity cost of producing one computer is ________ pounds of beef.

Art's opportunity cost of producing one computer is ________ pounds of beef.

A. 1/50 B. 50 C. 1/100 D. 100

If the demand for a firm's output is perfectly elastic, then the firm's Lerner Index equals

A) zero. B) one. C) infinity. D) one-half.