What is a marginal cost?

What will be an ideal response?

Marginal cost is the additional cost associated with continuing with an activity.

You might also like to view...

Which of the following statements concerning a monopolist is FALSE?

A) A monopolist will produce at which MR = MC. B) For a monopolist, marginal revenue is less than price. C) A monopolist will charge the highest price at which any individual will purchase the product. D) A monopolist will shut down if price is less than average variable cost.

Special interest groups are a determent to the political process.

A. True B. False C. Uncertain

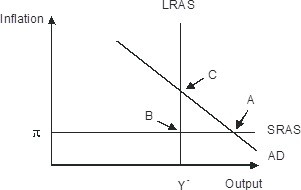

Refer to the figure below. In response to gradually falling inflation, this economy will eventually move from its short-run equilibrium to its long-run equilibrium. Graphically, this would be seen as

A. long-run aggregate supply shifting leftward B. Short-run aggregate supply shifting upward C. Short-run aggregate supply shifting downward D. Aggregate demand shifting leftward

Suppose the Fed implements a monetary expansion that is at least partially unexpected. Explain what effect this will have on stock prices

What will be an ideal response?