When goods do not have a price, which of the following primarily ensures that the good is produced?

a. buyers

b. sellers

c. government

d. the market

c

You might also like to view...

What is a centrally planned economy?

What will be an ideal response?

Instrumental Variables regression uses instruments to

A) establish the Mozart Effect. B) increase the regression R2. C) eliminate serial correlation. D) isolate movements in X that are uncorrelated with u.

A market that has no barriers to entry and many small firms selling products that are slightly different from one another is best described as:

A. oligopoly. B. perfect competition. C. monopolistic competition. D. monopoly.

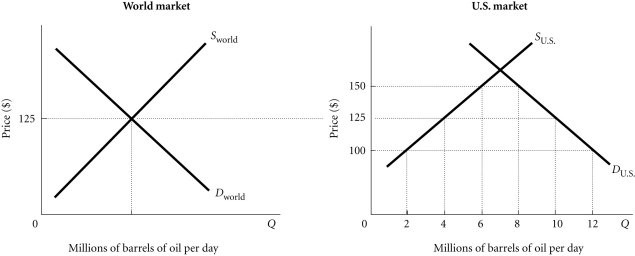

Refer to the information provided in Figure 4.4 below to answer the question(s) that follow. Figure 4.4Refer to Figure 4.4. Assume that initially there is free trade. Tariff revenue of $50 million per day will be generated if the United States imposes a ________ tariff per barrel on imported oil.

Figure 4.4Refer to Figure 4.4. Assume that initially there is free trade. Tariff revenue of $50 million per day will be generated if the United States imposes a ________ tariff per barrel on imported oil.

A. $25 B. $50 C. $100 D. $150