A market is said to "clear" when

A) sellers give up selling their goods because they can't find any buyers.

B) buyers and sellers are able to buy and sell as much as they want at the market price.

C) the government decides to shut it down.

D) sellers run out of goods to sell.

B

You might also like to view...

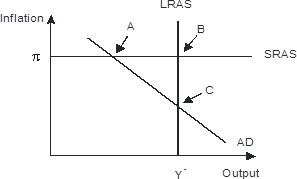

Refer to the figure below. In response to gradually falling inflation, this economy will eventually move from its short-run equilibrium to its long-run equilibrium. Graphically, this would be seen as

A. long-run aggregate supply shifting leftward B. Short-run aggregate supply shifting downward C. Aggregate demand shifting rightward D. Aggregate demand shifting leftward

The law of increasing costs holds that the opportunity cost:

a. of a good decreases as the quantity of the good produced increases. b. of a good is proportional to the resources used in its production. c. of a good increases as more of the good is produced. d. of a good does not change with the resources used its production. e. changes as more of the good is produced.

An externality is defined as

a. an opportunity cost that is not considered, which causes inefficiency. b. a social cost that affects parties external to a transaction. c. a transaction which imposes a loss on one of the parties involved. d. a "cost of doing business" that cannot be allocated to any particular good. e. the increase in cost associated with increased production.

A payoff matrix shows:

A. the demand curve facing a firm when there are only two firms. B. the payoff to being a perfectly competitive firm. C. the payoffs for each possible combination of strategies. D. the payoff to being a monopolist.