How is it that economists can claim that perfectly competitive markets give people what they want?

What will be an ideal response?

Because perfectly competitive firms will produce as long as the price of their product is greater than the marginal cost of production, they will continue to produce as long as a gain for society is possible. The market thus guarantees that the right things are produced.

You might also like to view...

A record of all transactions between residents of the reporting country and residents of the rest of the world over a period of time is called the:

A) national income product accounts. B) balance of payments accounting system. C) accrual accounting system. D) none of the above.

Which of the following can be considered an example of cyclical unemployment?

a. A recent graduate searching for his first job b. A ski instructor looking for a part-time job during the summer c. An engineer looking for a new job after losing his job during a recession d. A typist looking for a new job as his skills are not needed in the current labor market

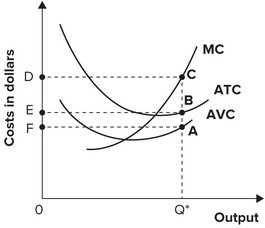

Refer to the graph shown. Total fixed cost of producing Q* is represented by:

A. area ABEF. B. area ACDF. C. area 0Q*AF. D. cannot be determined.

Given a market equilibrium point, explain, using the concepts of demand and supply, how it is achieved

What will be an ideal response?