The process by which inputs are transformed to outputs is referred to as:

A) production.

B) distribution.

C) depreciation.

D) absorption.

A

You might also like to view...

In a market for apples, a consumer purchases 30 pounds when the price of apples is $1 per pound and the consumer's income is $5,000 per month

When the price of apples increases to $2 per pound, without any change in the consumer's income, he decides to purchase only 15 pounds of apples. Suppose, after a given period of time, the consumer's income falls to $3,000 per month. His consumption of apples also decreases to 10 pounds. Using a graph, illustrate the difference between change in quantity demanded and the change in demand for apples.

Which of the following will most likely cause an outward shift in the production possibilities curve?

a. a reduction in the man-made productive resources available to the economy as the result of a decline in investment b. an increase in government payments to farmers for taking land out of production c. an increase from 40 to 50 hours in the average number of hours worked per week d. None of the above would cause an outward shift in the production possibilities curve.

It takes Heather 1 hour to change the oil in the car and 20 minutes to do the dishes. It takes Zach 1.5 hours to change the oil in the car. For Zach to have a comparative advantage changing the oil it must take him more than ______ minutes to do the dishes

Fill in the blank(s) with correct word

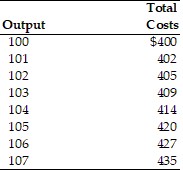

Refer to the above table. If the price is $3, the perfectly competitive firm should produce

Refer to the above table. If the price is $3, the perfectly competitive firm should produce

A. 104 units. B. 105 units. C. 103 units. D. 102 units.