If marginal cost is increasing, what do we know about average cost?

A. Average cost is constant and always lower than marginal cost because of the law of decreasing marginal productivity. As more items are produced, marginal costs increase (the same as productivity decreasing), but average costs remain constant because the total number of items produced is also increasing.

B. If marginal cost is increasing, average costs are rising. As the cost of the next item produced rises, the average cost of all items produced must also rise.

C. If marginal cost is increasing, average costs could be rising, falling, or constant. The direction of average costs depends on whether marginal cost is higher or lower than average cost.

D. If marginal cost is increasing, average costs are falling. Marginal costs only increase at very high levels of production. When items are mass-produced (because of economies of scale), their average costs always fall, even when marginal costs begin to increase.

Ans: C. If marginal cost is increasing, average costs could be rising, falling, or constant. The direction of average costs depends on whether marginal cost is higher or lower than average cost.

You might also like to view...

In the Keynesian model, a build-up of unwanted inventories leads to

A) rising interest rates. B) falling unemployment. C) falling output. D) falling money wages.

Suppose an airline company has several empty seats on a flight and the full price of an air ticket is $500 while the marginal cost per passenger is $100. The flight leaves in one hour. Which of the following actions will be the best profitable way to to ensure the remaining seats are sold?

What will be an ideal response?

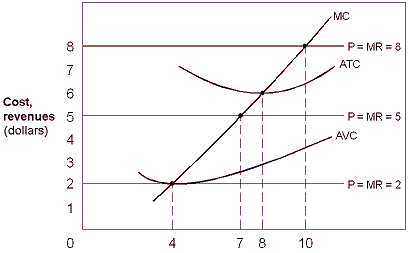

Exhibit 7-11 A firm's cost and marginal revenue curves

?

In Exhibit 7-11, when the price is $5, the firm:

In Exhibit 7-11, when the price is $5, the firm:

A. is making an economic profit of $21. B. should produce output equal to 10. C. is breaking even. D. should produce output equal to 7.

(Last Word) Theft and burglary:

A. can be viewed as attempts to maximize utility, given certain marginal costs and marginal benefits. B. are examples of irrational behavior. C. are applications of the law of increasing opportunity cost. D. are less economically rational than crimes of passion and violence.