All of the following are characteristics of a perfectly competitive industry EXCEPT

A. firms in the industry are price takers.

B. there are a large number of buyers and sellers with only a few being able to influence the market price.

C. the product sold is homogeneous.

D. buyers and sellers have equal access to information.

Answer: B

You might also like to view...

The total cost of producing a given level of output is

A) maximized when a corner solution exists. B) minimized when the ratio of marginal product to input price is equal for all inputs. C) minimized when the marginal products of all inputs are equal. D) minimized when marginal product multiplied by input price is equal for all inputs.

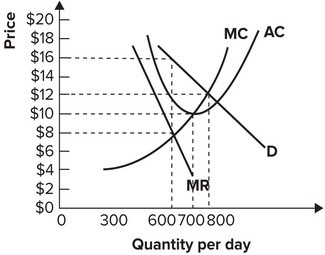

Refer to the graph shown. Assuming that this monopolist maximizes profit, the marginal cost of its last unit of output will be:

A. $10. B. $12. C. $16. D. $ 8.

A capital gain is defined as

A) the tax paid when one sells an asset. B) the positive difference between the sale price and the purchase price of an asset. C) the tax rate one pays when one moves into a higher tax bracket. D) an unanticipated increase in income.

An insurance company provides liability insurance to a restaurant protecting the owner against claims from customers. One area of coverage is protection against food poisoning claims. The insurance company may periodically send an employee into the restaurant to observe food preparation and food storage processes. The insurance company is trying to avoid:

A. transaction costs. B. moral hazard. C. adverse selection. D. free riding.