If the price of a one good increases and the quantity demanded of a different good decreases, then these two goods are

A) substitutes.

B) normal goods.

C) inferior goods.

D) inelastic goods.

E) complements.

E

You might also like to view...

Explain which of the following count as money

a. a check in Ann's checkbook b. currency in Ann's bank c. currency in Ann's purse d. Ann's checking deposit

On-the-job experience causes labor productivity to increase through an improvement in human capital

a. True b. False Indicate whether the statement is true or false

So far this year prices have been up __% over last year's prices.

Fill in the blank(s) with the appropriate word(s).

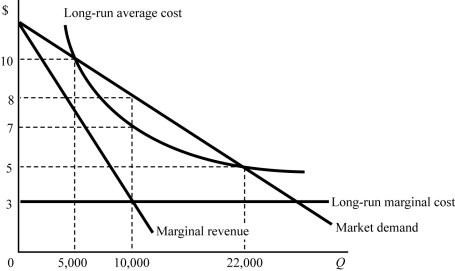

Figure 8.12 shows a demand and costs of an unregulated monopoly. This firm must:

Figure 8.12 shows a demand and costs of an unregulated monopoly. This firm must:

A. be a natural monopoly. B. have an exclusive government license. C. be a monopoly because it has a patent. D. be operating in a contestable market.