The term opportunity cost refers to the

a. value of what is gained when a choice is made.

b. difference between the value of what is gained and the value of what is forgone when a choice is made.

c. value of what is forgone when a choice is made.

d. direct costs involved in making a choice.

c

You might also like to view...

Gross Domestic Product in 2017 is more than five times larger than it was in 1960 but it is important to note that

A. none of the growth represented additional output of goods and services. B. this measurement of output fails to account for any of the effects of inflation. C. the population also grew substantially over the same time period. D. available graphs of output are unable to display such growth.

Assume you have an income of $200 and you can only purchase two goods – good A and good B

If the price of good A and B are $1 and $2 how much of each good can purchase? Assume that the price of good A falls why would you now consider not only consuming more of good A but also more of good B? What's going on that might cause this behavioral response?

When the quality of a good improves while its price remains the same, the purchasing power of the dollar

a. increases, so the CPI overstates the change in the cost of living if the quality change is not accounted for. b. increases, so the CPI understates the change in the cost of living if the quality change is not accounted for. c. decreases, so the CPI overstates the change in the cost of living if the quality change is not accounted for. d. decreases, so the CPI understates the change in the cost of living if the quality change is not accounted for.

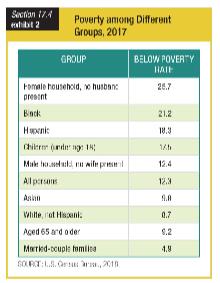

Based on the table showing poverty for different groups, which racial group has the highest poverty rate?

a. Asians

b. Blacks

c. Hispanics

d. Whites