If supply rises, what happens to equilibrium price and quantity?

What will be an ideal response?

price falls; quantity rises

You might also like to view...

Redbox rents DVDs. Other things constant, which of the following would likely increase the demand for their DVDs?

A) A rise in the cost of going to the movies B) A fall in the price of DVD players C) A fall in the price of Redbox DVD movie rentals D) Both A and B

Blank DVDs and prerecorded DVDs are substitutes in production. An increase in the price of a blank DVD will lead to

A) an increase in the supply of prerecorded DVDs. B) a decrease in the supply of prerecorded DVDs. C) an increase in the quantity supplied of prerecorded DVDs but not in the supply of prerecorded DVDs. D) a decrease in the quantity supplied of prerecorded DVDs but not in the supply of prerecorded DVDs.

At the current level of output, long-run marginal cost is $50 and long-run average cost is $75. This implies that:

A) there are neither economies nor diseconomies of scale. B) there are economies of scale. C) there are diseconomies of scale. D) the cost-output elasticity is greater than one.

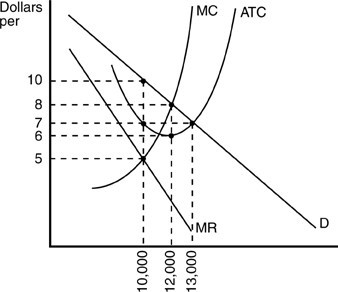

The above figure shows the situation of a monopolistic competitor in the short run. To maximize profits, the firm should produce

The above figure shows the situation of a monopolistic competitor in the short run. To maximize profits, the firm should produce

A. 12,000 units. B. 10,000 units. C. 13,000 unit. D. somewhere between 10,000 and 12,000 units.