Suppose a large firm allows its employees to choose whether to participate in its health insurance plan. The firm is trying to decide between two plans: Plan I has a low monthly premium but a high deductible, and Plan II has a high monthly premium but a

low deductible. Under which plan is adverse selection likely to be a bigger problem?

A) Plan I because it is likely to draw participants who expect high medical costs. This group expects to consume much health care services and therefore prefer low deductibles.

B) Plan II because it is likely to draw participants who expect high medical costs. Healthy individuals who do not expect to consume much health care services will not be willing to pay the high premiums.

C) Plan I because it is likely to draw the relatively healthy employees who do not expect to spend much on health care. Because the monthly premiums are low, the insurance company has to bear a bigger financial burden in the event of serious illnesses.

D) Plan II because it is likely to draw employees who tend to over-consume health care services because of the low deductible. Insurance companies are likely to end up paying out more claims than the premiums they collect.

Answer: B

You might also like to view...

Long-run diseconomies of scale exist over the range of output for which the long-run average total cost curve

a. rises. b. remains constant. c. falls. d. does not exist.

Which of the following measures of fit penalizes a researcher for estimating many coefficients with relatively little data?

A. Adjusted R-square B. R-square C. t-statistic D. Neither the t-statistic, the R-square, nor the adjusted R-square

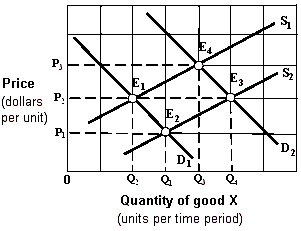

Exhibit 4-2 Supply and demand curves The market shown in Exhibit 4-2 is initially in equilibrium at point E3. Union negotiations for workers producing good X result in a wage increase. Other things being equal, which of the following is the new equilibrium after this wage increase is in effect?

The market shown in Exhibit 4-2 is initially in equilibrium at point E3. Union negotiations for workers producing good X result in a wage increase. Other things being equal, which of the following is the new equilibrium after this wage increase is in effect?

A. E1. B. E2. C. E3. D. E4.

The decision by firms of the quantity of output to supply is based on

A. the price of inputs. B. the price of output. C. government oversight. D. techniques of production available.