Answer the following statement true (T) or false (F)

1) The real opportunity cost of producing product X is the amounts of products Y, Z, and so forth,

that might have been produced if resources had not been used to produce X.

2) The short run is a period of time during which all costs are fixed costs.

3) Variable costs are costs that change directly with output.

4) Diseconomies of scale stem primarily from the difficulties in managing and coordinating a

large-scale business enterprise.

5) At zero units of output a firm's variable costs are zero.

1) T

2) F

3) T

4) T

5) T

You might also like to view...

Explain why one can write the demand for money as the price level times a function of the interest rate and real income as follows: = PxL (R, Y)

What will be an ideal response?

When calculating the price elasticity of demand, which of the following conditions must be satisfied?

A) All other factors that influence demand must be held constant. B) Prices of related goods must be held constant but all other factors must be allowed to vary. C) Prices of related goods must be allowed to vary but all other factors must be held constant. D) All other factors than influence demand must be allowed to vary.

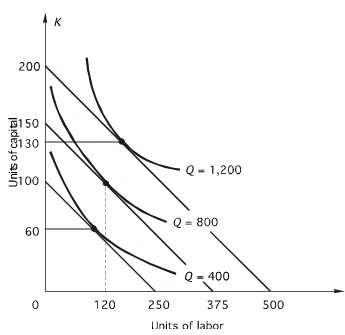

Refer to the following figure. The price of capital is $50 per unit: What is the minimum cost of producing 1,200 units of output?

What is the minimum cost of producing 1,200 units of output?

A. $7,000 B. $8,000 C. $9,000 D. $10,000 E. $11,000

A decrease in the real interest rate in the U.S. will cause net exports to:

A. increase because exports will remain constant but imports will decrease. B. decrease because exports will increase but imports will increase. C. increase because exports will increase and imports will decrease. D. decrease because exports will decrease and imports will increase.