Suppose that in a market for used cars, there are good used cars and bad used cars (lemons). Consumers are willing to pay as much as $6,000 for a good used car but only $1,000 for a lemon

Sellers of good used cars value their cars at $5,000 each and sellers of lemons value their cars at $800 each. Buyers cannot tell if a used car is reliable or is a lemon. Based on this information, what is the likely outcome in the market for used cars?

A) Most used cars offered for sale will be lemons.

B) Both good used cars and lemons will sell for $4,500 each.

C) Only lemons will sell, for $800 each.

D) Both good used cars and lemons will sell for $1,000 each.

A

You might also like to view...

The effective rate of protection is

(a) value added with protection divided by value added without protection. (b) value added with protection. (c) value added without protection. (d) (value added with protection minus value added without protection) divided by value added without protection.

Which of the following statements is true?

A) Keynes believed wages are inflexible downward but prices (of goods and services) are flexible. B) Keynes believed an economy could get stuck in a recessionary gap. C) Keynes originated the idea of efficiency wages. D) Keynes believed the economy is self-regulating. E) b and c

To avoid subsidies, the government should cap the price for natural monopolies at their:

A. marginal cost. B. fixed cost. C. average total cost. D. average variable cost.

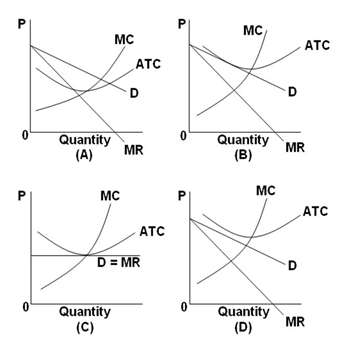

Refer to the below graphs. A short-run equilibrium that would produce losses for a monopolistic ally competitive firm would be represented by graph:

A. A

B. B

C. C

D. D