A constant-cost industry is an industry in which

A) average costs fall as the industry expands output.

B) input prices rise at a constant rate as firms in the industry use more inputs.

C) average costs rise as the industry expands output.

D) average costs remain constant as the industry expands output.

D

You might also like to view...

If in some range of production, average cost is falling, the firm is experiencing

A. increasing returns to scale. B. decreasing returns to scale. C. constant returns to scale. D. increasing costs per unit of output.

GDP overstates the productive capacity of a country when:

a. economic bads like pollution are produced and then must be cleaned up. b. there is a sizable underground economy. c. nonmarket production represents a large portion of the economy. d. working conditions improve, allowing jobs to be completed safer and faster.

Which of the following were invented centuries ago in China?

a. gunpowder b. the wheelbarrow c. printing with movable type d. all of the above

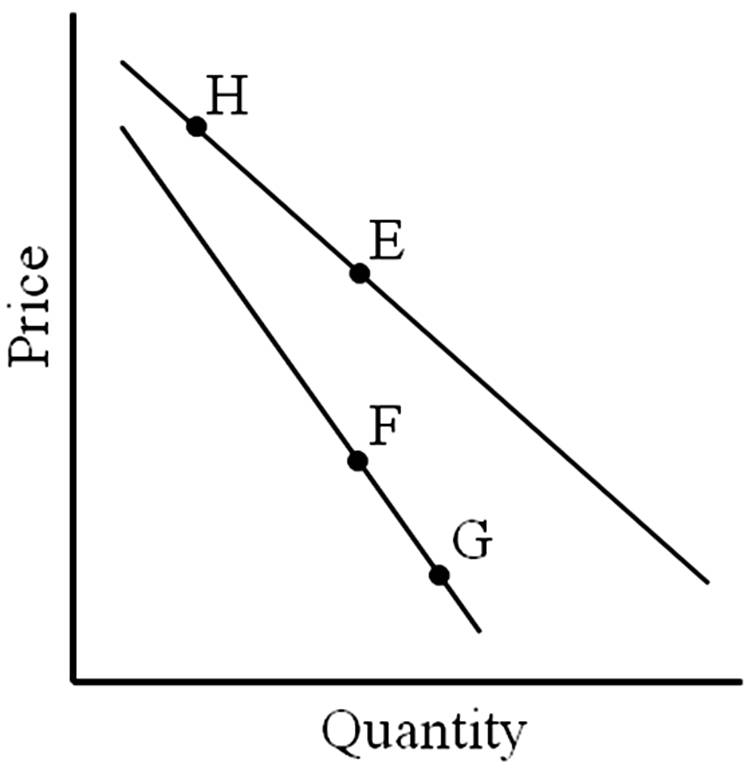

A move from E to F represents

A. an increase in quantity demanded.

B. a decrease in quantity demanded.

C. an increase in demand.

D. a decrease in demand.