In the long run, firms in a perfectly competitive market choose to produce a quantity:

A. that does not cover minimum average variable costs.

B. where marginal costs are less than average variable costs.

C. that earns zero economic profits.

D. where ATC and AVC are at their minimum values.

Answer: C

You might also like to view...

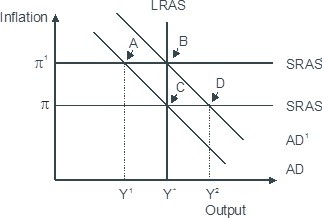

Based on the figure below. Starting from long-run equilibrium at point C, a tax cut that increases aggregate demand from AD to AD1 will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C B. B; C C. B; A D. D; B

In the above figure, the sum of real planned investment spending, government expenditures, and net export spending is equal to

A) $0.5 trillion. B) $1.0 trillion. C) $1.5 trillion. D) $2.0 trillion.

If large numbers of young Americans thought the life of a cowhand was great (despite the hardships), we would expect

a. an increase in the wages of cowhands. b. a decrease in the wages of cowhands because demand would be reduced. c. no impact on wages, which are determined by supply and demand, not preferences. d. a decrease in the wages of cowhands because supply would be enlarged.

Toyota has been successful in Europe by exporting cars to Europe as well as designing and manufacturing cars in Europe for the European market.

a. true b. false