Economists use the term variable costs to refer to

a. prices of inputs that are subject to sudden change, like fuel.

b. an increase in the price of any input.

c. costs that vary with the type of final product being produced.

d. costs that vary with the quantity of output produced.

d. costs that vary with the quantity of output produced.

You might also like to view...

In order to spend more time with her children, a young mother decides to work less hours as her pay increases. What does her labor supply curve look like?

What will be an ideal response?

Describe the behavior of the unemployment rate from the early 1990's to the present.

What will be an ideal response?

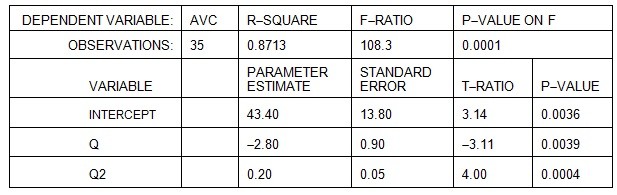

Straker Industries estimated its short-run costs using a U-shaped average variable cost function of the formAVC = a + bQ + cQ2and obtained the following results. Total fixed cost (TFC) at Straker Industries is $1,000.  At what level of output is average variable cost (AVC) at its minimum point for Straker Industries?

At what level of output is average variable cost (AVC) at its minimum point for Straker Industries?

A. 7 B. 14 C. 0.14 D. 28 E. 4.7

If a firm is producing the level of output at which short-run average cost equals long-run average cost, then

A. the firm has chosen the cost-minimizing combination of inputs to produce this level of output. B. the firm has chosen the profit-maximizing level of output. C. with a fixed amount of capital, short-run average cost is greater than long-run average cost at any other level of output. D. both a and b E. all of the above