In economics, secondary effects refer to the

a. value of the goods that an individual must give up as the result of choosing an alternative.

b. indirect effects that often result from an action or policy change.

c. immediate and highly visible intended consequences of an action or policy change.

d. value of a good derived by the consumer.

b. indirect effects that often result from an action or policy change.

You might also like to view...

The horizontal summation of all individual quantities demanded at different given prices results in the

A. market supply curve. B. market demand curve. C. individual demand curve. D. equilibrium demand and supply curves.

If demand for a good is perfectly inelastic, then

A. a price increase would cause a fall in total revenue. B. a price increase would cause no change in quantity demanded. C. a price increase would cause an increase in quantity demanded. D. a price increase would cause a fall in quantity demanded.

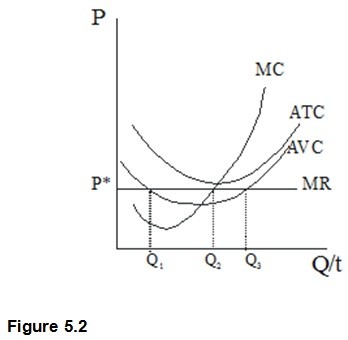

In Figure 5.2, what output would a perfect competitor produce?  Figure 5.2

Figure 5.2

A. Q1 B. Q2 C. Q3 D. 0

The era of free agency brought salaries closer to

A. their long run average. B. their universally agreed-upon, morally-justifiable level. C. the reservation wage of players. D. the marginal revenue product of players.