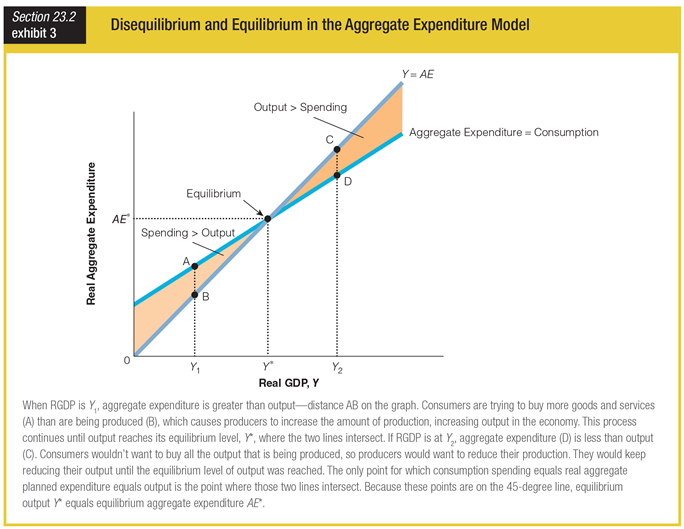

If consumption is at point A, producers will increase output to equal what level?

a. B

b. C

c. D

d. E (Equilibrium)

d. E (Equilibrium)

You might also like to view...

The short-run aggregate supply curve in modern Keynesian analysis is

A) downward sloping. B) horizontal. C) vertical. D) upward sloping.

Answer the following statements true (T) or false (F)

1) If the market price is $2 and a perfectly competitive firm is producing 1,000 units and the marginal cost to produce the 1,000th unit is $2, the difference between marginal revenue and marginal cost (MR - MC) is zero. 2) Overexpansion can bankrupt a perfectly competitive firm. 3) If the market price is $3 and a perfectly competitive firm is producing 1,400 units and the marginal cost to produce the 1,400th unit is $2, the difference between marginal revenue and marginal cost (MR - MC) is zero. 4) If the market price is $1 and a perfectly competitive firm is producing 1,500 units and the marginal cost to produce the 1,500th unit is $2, the difference between marginal revenue and marginal cost (MR - MC) is negative. 5) If the market price is $4 and a perfectly competitive firm is producing 1,500 units and the marginal cost to produce the 1,500th unit is $3.50, the difference between marginal revenue and marginal cost (MR - MC) is negative.

A test was scheduled for Monday morning, but you went to a party on Saturday night. If you hadn't attended the party, you could have studied for the test or gone to a movie. Which of the following is true?

a. The opportunity cost of going to the movie is studying for the test. b. The opportunity cost of going to the party is the movie. c. The opportunity cost of going to the party is both the movie and the study time. d. Because you could go to the party only that night but could go to a movie any time, the opportunity cost of the party is the study time. e. From the above information, it's not possible to determine the opportunity cost of attending the party.

The production possibilities curve illustrates which two of the following essential principles?

A. Economic growth and market failure. B. Factors of production and price signals. C. Market mechanisms and laissez faire. D. Scarce resources and opportunity cost.