Suppose you operate in a monopolistically competitive market. If you sell your good at a price of $20 and your average cost of production is $15:

A. your market may be in long-run equilibrium.

B. you cannot be in short-run equilibrium.

C. you should expect competing firms to enter your market and shift the demand curve for your good to the left.

D. you should expect competing firms to enter your market and shift the demand curve for your good to the right.

Answer: C

You might also like to view...

The table below shows the weekly supply for hamburgers in a market where there are just three sellers.PriceSeller 1 Qs 1Seller 2 Qs 2Seller 3 Qs 3$5854464334322221If the price of a hamburger increases from $2 to $4, then the weekly market quantity of hamburgers supplied will

A. increase from 5 to 13. B. decrease from 9 to 5. C. decrease from 13 to 5. D. increase from 5 to 9.

Monopolistically competitive markets feature heterogeneous products.

Answer the following statement true (T) or false (F)

Which of the following government programs will create a surplus?

A. rent control B. the minimum wage law C. usury laws D. price controls on oil

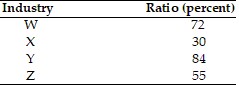

Four-Firm Concentration Ratios The most oligopolistic industry of those presented in the above table is likely to be industry

The most oligopolistic industry of those presented in the above table is likely to be industry

A. W. B. X. C. Y. D. Z.