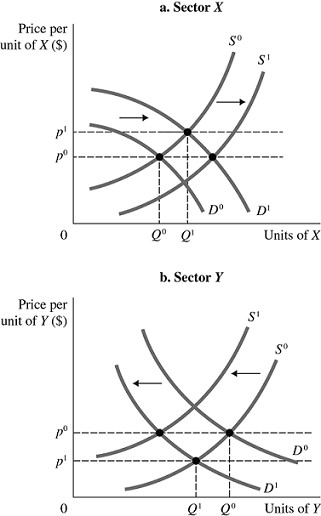

Refer to the information provided in Figure 12.4 below to answer the question(s) that follow. Figure 12.4There are two sectors in the economy, X and Y, and both are in long-run, zero-profit equilibrium at the intersections of S0 and D0.Refer to Figure 12.4. Assume consumer preference changes toward X and away from Y. Ceteris paribus, the likely change in capital flows in sectors X and Y will eventually________ in industry X and ________ in industry Y.

Figure 12.4There are two sectors in the economy, X and Y, and both are in long-run, zero-profit equilibrium at the intersections of S0 and D0.Refer to Figure 12.4. Assume consumer preference changes toward X and away from Y. Ceteris paribus, the likely change in capital flows in sectors X and Y will eventually________ in industry X and ________ in industry Y.

A. increase the price to P1; increase the price to P0

B. decrease the price to P0; decrease the price to P1

C. increase the price to P1; decrease the price to P1

D. decrease the price to P0; increase the price to P0

Answer: D

You might also like to view...

A time series graph reveals whether there is a ________ , which represents ________

A) trends in two variables; unrelated variables B) relationship between two variables; a trend in a variable C) cross-section relationship; a general tendency for the variables to rise or fall D) trend in a variable; a general tendency for the variable to rise or fall E) relationship between two variables; a cross-section relationship

Which of the following are devices that the government uses to achieve a more efficient allocation of resources in the presence of external benefits?

A) taxes, private subsidies, and regulation B) public provision, taxes, and private subsidies C) regulations, public provision, and vouchers D) vouchers, public provision, and private subsidies E) public provision, taxes, and vouchers

From an initial long-run macroeconomic equilibrium, if the Federal Reserve anticipated that next year aggregate demand would grow significantly slower than long-run aggregate supply, then the Federal Reserve would most likely

A) decrease interest rates. B) decrease income tax rates. C) increase interest rates. D) increase income tax rates.

Which of the following best explains an economic criticism of unregulated monopolists?

A. Monopolists do not try to minimize their fixed costs of production. B. Monopolists produce where marginal revenue is greater than marginal costs. C. Monopolists attempt to produce too many products, and as a result, their prices are high, and consumer's waste time trying to choose between too many options. D. Monopolists restrict output, and as a result, they fail to produce units that are valued more than the marginal cost of producing them.