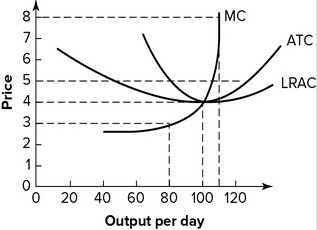

Refer to the graph shown, which depicts a perfectly competitive firm. If the price of the product is $8 and the firm maximizes profit:

A. output will be 100 units per day.

B. average cost of the product will be at the minimum possible level.

C. the firm will earn economic profits of more than $330 per day.

D. the industry will be in long-run equilibrium.

Answer: C

You might also like to view...

Suppose the economy is initially at equilibrium, in which total planned real expenditures equals real GDP. Which of the following will occur if there is an increase in autonomous investment?

A) Inventories will decrease immediately and production of goods and services will increase until real GDP catches up with total planned real expenditures. B) Inventories will increase immediately and production of goods and services will decrease until real GDP catches up with total planned real expenditures. C) Inventories will not change and production of goods and services will not change either. D) Both inventories and production of goods and services will increase.

When a physician knows more about alternative treatments than her patients, we say that _______ exists

a. rational ignorance. b. perfect information. c. asymmetric information. d. moral hazard. e. adverse selection.

Which theory does NOT support unrestricted free trade between countries

What will be an ideal response?

An increase in the reserve requirement:

A. increases the money supply, which leads to increased interest rates and a decrease in GDP. B. increases the money supply, which leads to decreased interest rates and a decrease in GDP. C. decreases the money supply, which leads to increased interest rates and a decrease in GDP. D. decreases the money supply, which leads to decreased interest rates and a decrease in GDP.