Firms in perfect competition are price takers because

A) one firm determines the price that all other firms in the industry will charge.

B) consumers have enough market power to set prices.

C) firms accept the price determined by the government.

D) each firm is too small relative to the market to be able to influence the price.

Answer: D

You might also like to view...

Governments sometime create an excess supply of a product by setting a minimum price that is greater than the equilibrium price, resulting in a permanent excess supply of the product. This is known as a price ceiling

Indicate whether the statement is true or false

Why do foreigners export goods and services to buyers in the United States?

What will be an ideal response?

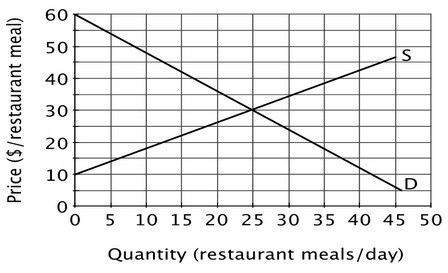

Refer to the accompanying figure. The equilibrium price in this market is ________ and the equilibrium quantity is ________.

A. $25; 25 B. $30; 25 C. $25; 30 D. $30; 30

Which one of the following is a source of conflict between owners and managers?

A. Managers and owners have a very short time horizon. B. Owners have short time horizons, while managers have to worry about future cash flows. C. Managers and owners worry about the entire future cash flows. D. Managers have short time horizons, while owners have to worry about future cash flows.