Average total cost is minimized in long-run equilibrium for a monopolistically competitive firm.

Answer the following statement true (T) or false (F)

False

You might also like to view...

Two parties can capture gains from specialization and trade whenever: a. One party is twice as good as producing all goods as the other

b. The opportunity costs of producing each good are the same for both parties. c. Both parties can produce equal amounts of both goods. d. None of the above are true.

Who is more likely to drive carelessly, Camila in her 1980 Ford with bad brakes or Samantha, who has a 2005 BMW with all the most recent safety options?

If the government imposes a price ceiling below the market equilibrium price, which of the following will result?

A. There will be a surplus of the good. B. The quantity demanded will exceed the quantity supplied. C. The quantity supplied will exceed the quantity demanded. D. The demand curve will shift to the left.

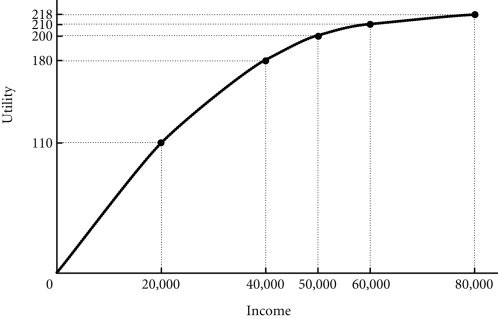

Refer to the information provided in Figure 17.1 below to answer the question(s) that follow.  Figure 17.1 Refer to Figure 17.1. Dmitri has two job offers when he graduates from college. Dmitri views the offers as identical, except for the salary terms. The first offer is at a fixed annual salary of $40,000. The second offer is at a fixed salary of $20,000 plus a possible bonus of $40,000. Dmitri believes that he has a 50-50 chance of earning the bonus. If Dmitri takes the offer that maximizes his expected utility and is he is risk averse, then

Figure 17.1 Refer to Figure 17.1. Dmitri has two job offers when he graduates from college. Dmitri views the offers as identical, except for the salary terms. The first offer is at a fixed annual salary of $40,000. The second offer is at a fixed salary of $20,000 plus a possible bonus of $40,000. Dmitri believes that he has a 50-50 chance of earning the bonus. If Dmitri takes the offer that maximizes his expected utility and is he is risk averse, then

A. he will take the first offer. B. he will take the second offer. C. he is indifferent between the offers-both yield the same expected utility. D. Indeterminate from the given information-we cannot say what he will do.