The marginal cost of a good is equal to the:

a. change in fixed costs as output changes

b. change in implicit costs as output changes.

c. change in variable costs as output changes.

d. change in opportunity costs as output changes.

c

You might also like to view...

In investment banking the "spread" is the difference between

A) the value of a firm's assets and the value of its liabilities. B) the bid and asked prices on a bond. C) the price of new capital guaranteed to the issuing firm and the price that can be obtained in the market. D) the price of a new stock issue and the price of an equivalent new bond issue.

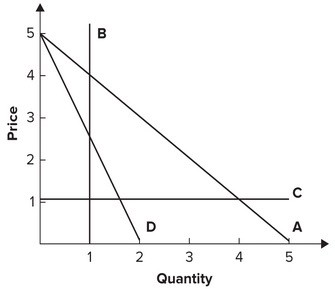

Refer to the following graph. Which of the following curves demonstrates a unit elastic demand curve? (That is, a curve where elasticity is 1 at each point.)

Which of the following curves demonstrates a unit elastic demand curve? (That is, a curve where elasticity is 1 at each point.)

A. A B. B C. C D. None of the answers is correct.

The United States is capable of producing many goods and services that it imports, but it does not because

A. We have lost those skilled workers. B. We can export goods that we specialize in. C. We produce those goods more cheaply if we make them ourselves. D. We can import those goods at a lower opportunity cost than if we make them ourselves.

Whenever average output produced per worker during a specific time-period increases, then

A. leisure time increases. B. nominal GDP decreases. C. the standard of living goes down. D. labor productivity increases.