Increasing cost industries are consistent with ________ in the long run.

A. the law of supply.

B. the law of diminishing marginal product.

C. the law of demand.

D. None of these are correct.

Answer: A

You might also like to view...

The above figure shows the market for buckets of golf balls at the driving range. A new leisure time tax is placed on suppliers in this market, shifting the supply curve from S0 to S1. The amount of this tax is ________ per bucket of golf balls

A) $4 B) $2 C) $2.50 D) $1 E) $3

When national output rises, the economy is said to be in

A) an expansion. B) a deflation. C) an inflation. D) a recession.

If the total cost of production for 1000 widgets is $2000 and marginal cost is constant at $1, what is the average fixed cost for the 1000 widgets?

A) $2 B) $1.50 C) $1 D) $0.50

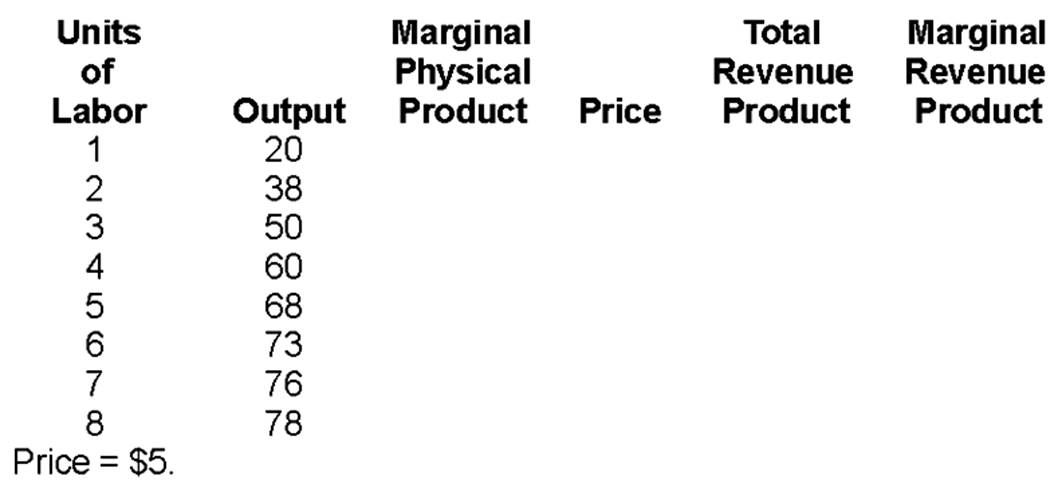

If the wage rate were $15, how many workers would be hired?