Cost

A) is what the buyer pays to get the good.

B) is always equal to the marginal benefit for every unit of a good produced.

C) is what the seller must give up to produce the good.

D) is greater than market price, which results in a profit for firms.

E) means the same thing as price.

C

You might also like to view...

Which of the following statements describes a basic difference in the economic effects of a tariff versus a quota?

A. A quota raises product prices, but a tariff does not. B. A quota reduces domestic consumption of the product, but a tariff does not. C. A tariff raises product prices, but a quota does not. D. A tariff allows imports to increase if demand increases, whereas a quota does not.

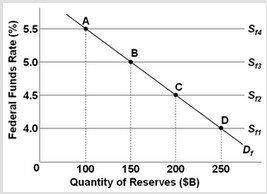

Use the following graph to answer the next question. If demand for overnight funds in the graph should increase by $50 billion at each and every point on the demand curve, but the Federal Reserve wants to keep the target rate at 5.0%, what will be the new equilibrium quantity of reserves?

If demand for overnight funds in the graph should increase by $50 billion at each and every point on the demand curve, but the Federal Reserve wants to keep the target rate at 5.0%, what will be the new equilibrium quantity of reserves?

A. $200 billion B. $100 billion C. $150 billion D. $250 billion

If a perfectly competitive firm faces a price below its average total cost but above the shutdown point, it should stay open

a. True b. False Indicate whether the statement is true or false

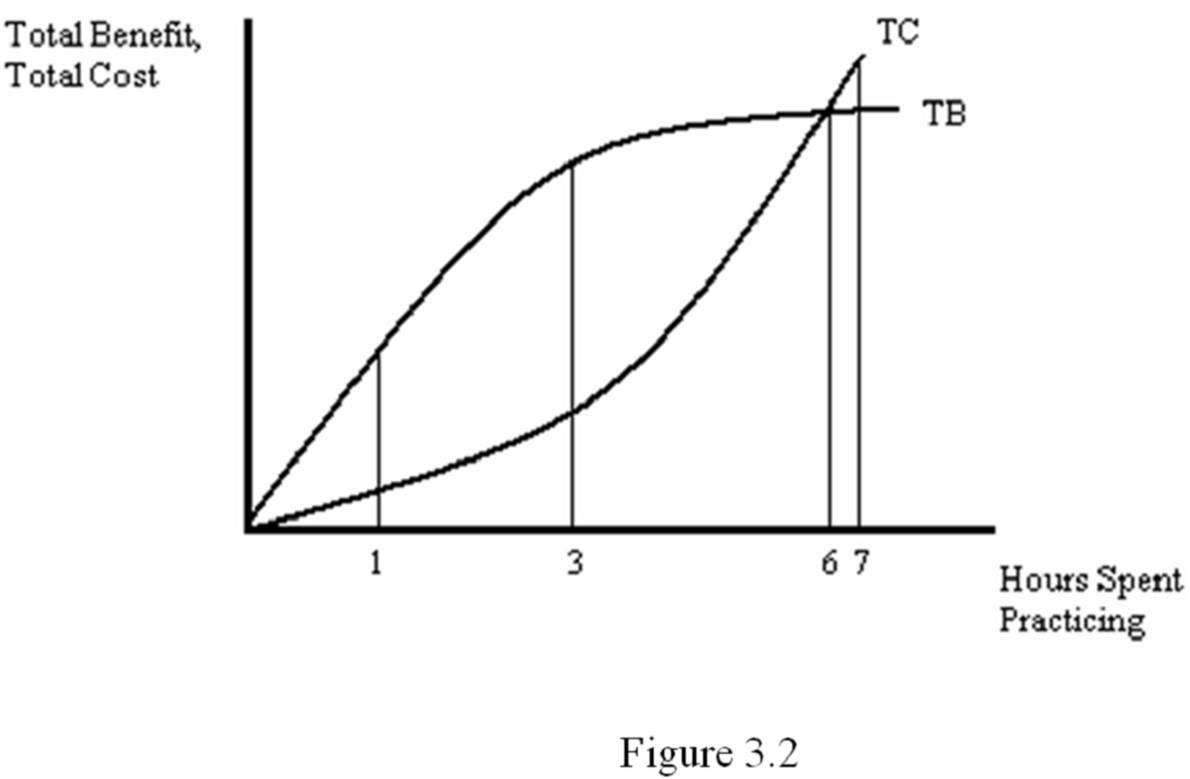

Figure 3.2 shows the total cost and total benefit curves for a professional guitarist. According to the graph, which of the following is the best number of hours the guitarist should spend practicing each day?

A. 3

B. 4

C. 6

D. 7