A production possibilities curve that is a straight line represents the case of

A) constant costs.

B) increasing costs.

C) decreasing costs.

D) constant opportunity costs but increasing real costs.

E) constant opportunity costs but decreasing real costs.

A

You might also like to view...

A decrease in AS will trigger less inflation under which of the following conditions?

A. AD is relatively steep. B. AD is relatively flat. C. AS is relatively steep. D. AS is relatively flat.

The academic calendar for a university is August 15 through May 15. A professor commits to a contract that binds her to a teaching position at this university for this period. Based on this? information, the short run for the professor

A. will be the nine month period between August 15 and May? 15; any time period longer than this will be long run for her. B. will be the time period between August 15 and December? 31; any time period longer than this will be long run for her. C. will be the calendar year between January 1 and December? 31; any time period longer than this will be long run for her. D. will be the time period between August 15 of the current year and August 14 of the following? year; any time period longer than this will be long run for her.

According to the income effect of labor supply, if leisure is a normal good, then an increase in the wage rate will ________ the quantity of labor ________.

A. increase; supplied B. decrease; supplied C. increase; demanded D. decrease; demanded

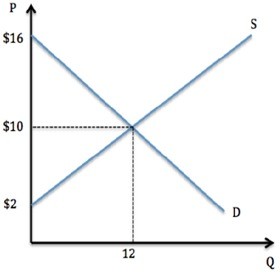

Assume the market was in equilibrium in the graph shown. If the market price were set to $6, which of the following is true?

Assume the market was in equilibrium in the graph shown. If the market price were set to $6, which of the following is true?

A. For those still interacting in the market, some surplus is transferred from seller to buyer. B. Producers gain the surplus of those buyers who dropped out of the market. C. For those still interacting in the market, some surplus is transferred from buyer to seller. D. Consumers gain the surplus of those sellers who dropped out of the market.