In a perfectly competitive market, firms will exit in the

a. short run if they are suffering economic losses

b. short run if they are earning below-normal profit

c. short run if price exceeds average total cost

d. long run if they are earning above-normal profit

e. long run if they are suffering economic losses

E

You might also like to view...

The apple market is perfectly competitive and is in long-run equilibrium. Now a disease kills 50 percent of the apple orchards. In the short run, the price of a bag of apples ________ and the remaining apple growers make ________ economic profit

In the long run, the ________. A) increases; zero; price of apples will return to their original level B) remains the same; zero; orchards will be replanted and growers will make normal profits C) increases; zero; orchards will be replanted and economic profit will return to zero D) increases; positive; orchards will be replanted and economic profit will return to zero

At equilibrium expenditure...

a) consumers' expenditures on goods and services equal firms' purchases of investment goods b) firms hold no inventories of raw materials or final goods c) aggregate planned expenditure equals real GDP d) aggregate planned expenditure equals real GDP minus net exports

Trade can stifle the development of industries than might be more efficient than existing ones

Indicate whether the statement is true or false

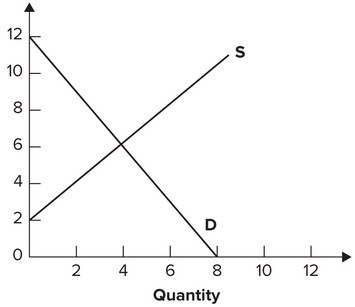

Refer to the graph shown. If the government imposed a price ceiling of $4, consumer surplus would:

A. fall from 12 to 4. B. rise from 12 to 13. C. be unchanged at 12. D. fall from 12 to 8.