What two factors are the keys to determining labor productivity?

A) technology and the quantity of capital per hour worked

B) the growth rate of real GDP and the interest rate

C) the average level of education of the workforce and the price level

D) the business cycle and the growth rate of real GDP

A

You might also like to view...

Refer to Figure 12-5. The figure shows the cost structure of a firm in a perfectly competitive market. If the firm's fixed cost increases by $1,000 due to a new environmental regulation, what happens to its profit-maximizing output level?

A) It remains the same. B) It decreases. C) It increases. D) It could increase, decrease, or remain constant, depending on whether the firm is able to cut costs somewhere else.

Most voters will likely be concerned with

What will be an ideal response?

Can a firm experience diminishing returns in the long run?

What will be an ideal response?

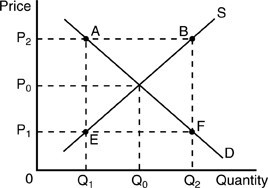

Refer to the above figure. Other things being equal, if price is at P2, then we would expect

Refer to the above figure. Other things being equal, if price is at P2, then we would expect

A. consumers to reduce their offering price for the good. B. consumers to bid against each other for goods and force the price still higher. C. an excess quantity demanded to occur. D. price to decline until an equilibrium is achieved at P0.