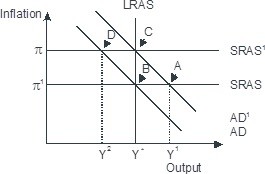

Based on the figure below. Starting from long-run equilibrium at point C, a tax increase that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C

B. D; B

C. A; B

D. B; C

Answer: B

You might also like to view...

Compared to a permanent reduction in tax rates, a temporary tax cut will generally

a. exert a larger impact on output and employment because its effects are immediate, long-lasting, and do not add much to the national debt. b. exert a smaller impact on output and employment because the temporary cut will not exert much impact on long-term income or the incentive to earn. c. exert a larger impact on output and employment because the temporary tax cut will lead to a larger budget deficit. d. exert an identical impact on output and employment because the incentive effects will be the same regardless of whether the tax cut is temporary or permanent.

Eliminating double-taxation would likely

a. raise saving and primarily benefit people with lower incomes. b. raise saving but primarily benefit people with higher incomes. c. reduce saving but primarily benefit people with lower incomes. d. reduce saving and primarily benefit people with higher income.

Relative to a single price monopolist, a price discriminating monopolist generates:

A. less total surplus. B. more total surplus. C. the same amount of total surplus, but less consumer surplus and more producer surplus. D. the same amount of total surplus, but more consumer surplus and less producer surplus.

Suppose your firm is operating in a perfectly competitive market, and that the minimum average variable cost of producing your good is $30. If the price of the good is $32, your firm should:

A. not produce anything since the price is above the minimum of average variable cost. B. not consider price when determining the amount to sell. C. supply the amount of the good where the marginal cost of production is equal to $32. D. supply the amount of the good where the marginal cost of production is $30.