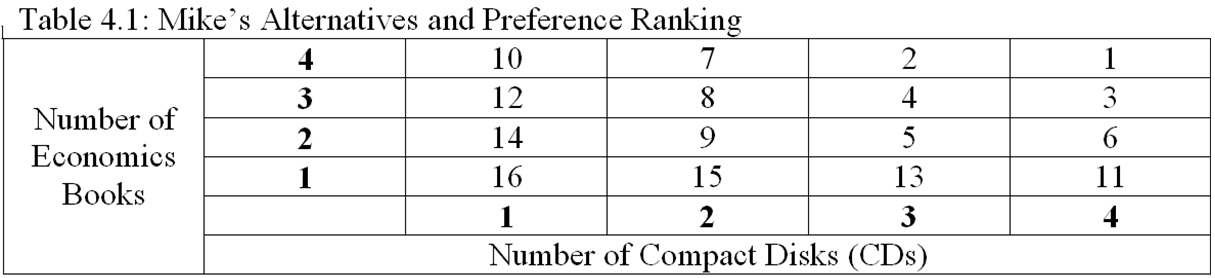

Refer to Table 4.1. If Mike starts with 4 CDs and 1 economics book, would he be willing to trade one CD for two economics books?

A. Yes, because the bundle with 3 CDs and 3 economics books is ranked higher than the bundle with 4 CDs and 1 economics book

B. No, because the bundle with 3 CDs and 3 economics books is ranked higher than the bundle with 4 CDs and 1 economics book

C. Yes, because the bundle with 4 CDs and 1 economics book is ranked higher than the bundle with 3 CDs and 3 economics books

D. No, because the bundle with 4 CDs and 1 economics book is ranked higher than the bundle with 3 CDs and 3 economics books

A. Yes, because the bundle with 3 CDs and 3 economics books is ranked higher than the bundle with 4 CDs and 1 economics book

You might also like to view...

Consider the following:

(i) Suppose labor and capital are complements in production. Explain why a firm's long-run demand for labor is more elastic than its short-run demand. (ii) Suppose labor and capital are substitutes in production. Will the firm's long-run demand for labor still be more elastic than its short-run demand? Why or why not?

Usually an abundance of natural resources ________ labor productivity.

A. increases B. has no effect on C. decreases D. doubles

Define the quantity theory of money and show how it is related to the equation of exchange

What will be an ideal response?

The law of increasing costs means that when an economy increases the production of one item:

a) the opportunity cost goes up b) the actual cost of making the item goes down c) the actual cost goes up but the opportunity cost goes down d) the production costs will increase alot