After some point successive equal increases in a variable factor of production, when added to a fixed amount of inputs, will result in smaller increases in output. This is known as

A. marginal physical product.

B. the long run.

C. the law of diminishing marginal product.

D. short run average cost.

Answer: C

You might also like to view...

Which of the following will tend to occur when a surplus exists in a market?

A) supply will increase and demand will decrease until the surplus disappears. B) supply will decrease and demand will increase until the surplus disappears. C) the price will tend to rise over time. D) the price will tend to decrease over time.

Which of the following can be classified as a regressive tax?

a. Excise tax. b. Sales tax. c. Gasoline tax. d. All of these.

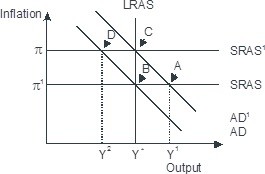

Based on the figure below. Starting from long-run equilibrium at point C, a decrease in government spending that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at__ creating _____gap.

A. B; no output B. D; an expansionary C. B; recessionary D. D; a recessionary

The marginal propensity to consume is calculated by dividing the change in consumer spending by the change in disposable income.

Answer the following statement true (T) or false (F)