Perfectly competitive firms are earning economic profits at a market price of $18 and an average total cost of $15. If new firms enter and increase the average total cost for all firms, the market price will ________ until ________.

A) fall; it reaches the new lower average total cost

B) increase; it reaches the new higher average total cost

C) fall; it reaches the new higher average total cost

D) increase; economic profits are equal to zero

C) fall; it reaches the new higher average total cost

You might also like to view...

Majority of international migrants move to:

A. The U.S. and Canada B. Western Europe C. Countries relatively close to their home countries D. Japan and Australia

Refer to above Table 2-2. What is the nominal GDP in year 2?

A) $18.60 B) $14.60 C) $18.00 D) 400 units

Which of the following is not one of the three pillars of productivity growth?

a. rate of capacity utilization b. rate of technological improvement c. rate of improvement in workforce quality d. rate of capital expansion

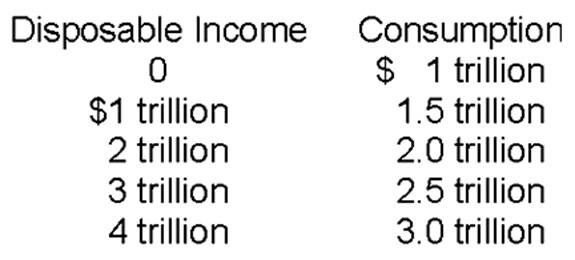

How much is the marginal propensity to consume when disposable income rises from 0 to $1 trillion?

A. 0

B. .25

C. .5

D. .75