Answer the following questions true (T) or false (F)

1. Market equilibrium occurs where supply equals demand.

2. A shortage occurs when the market price is lower than the equilibrium price.

3. A shortage is defined as the situation that exists when the quantity of a good supplied is greater than the quantity demanded.

1. FALSE

2. TRUE

3. FALSE

You might also like to view...

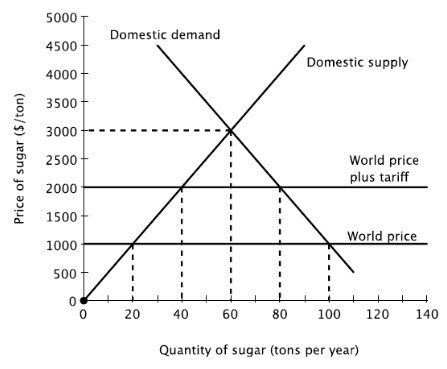

The amount of revenue the government collects after imposing the tariff is ________.

A. $40,000 B. $10,000 C. $1,000 D. $4,000

The law of demand states that

A) people demand less at lower prices. B) the quantity demanded is directly related to price. C) the quantity demanded is inversely related to price. D) changes in price and changes in quantity demanded move in the same direction.

If the demand curve for a good is horizontal and the price is positive, then a leftward shift of the supply curve results in

A) a price of zero. B) an increase in price. C) a decrease in price. D) no change in price.

Tom's Donuts can invest in a new espresso machine that costs $300 and will yield expected profits of $200 each year for two years. At lower interest rates, the present discounted value of profits from the investment

A. decreases. B. increases. C. is unchanged. D. is indeterminate from the given information.