Assume the firms in a perfectly competitive industry are initially in long-run equilibrium and the cost of labor increases. In the short run, this will cause firms in the industry to:

A) reduce output and incur a loss.

B) reduce output and earn a positive economic profit.

C) increase output and incur a loss.

D) increase output and earn a positive economic profit.

A

You might also like to view...

What happens to national saving when the government runs a budget surplus? What happens to national saving when the government runs a budget deficit?

What will be an ideal response?

Firms that emit toxins into the air:

a. underproduce because the private cost of production exceeds the social cost. b. overproduce because the social cost of production exceeds the private cost. c. produce the same as nonpolluting firms. d. produce at the socially optimal amount.

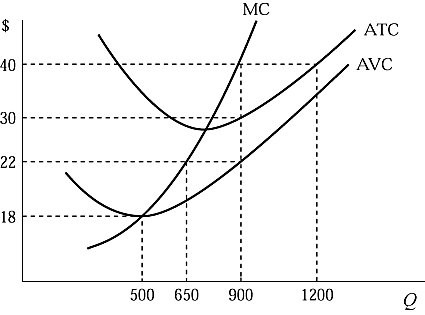

Figure 6.1 shows the cost structure of a firm in a perfectly competitive market. If the firm's fixed cost increases by 3,000 due to a new government regulation:

Figure 6.1 shows the cost structure of a firm in a perfectly competitive market. If the firm's fixed cost increases by 3,000 due to a new government regulation:

A. the marginal cost curve shifts upward. B. the average variable cost curve shifts upward. C. the average total cost curve shifts upward. D. None of these

How do economists view profits?

A. Profits are an asset the business holds. B. Profits are one of the costs paid to a factor of production. C. The firm's profit equals the sum of all payments to the 5 factors of production. D. Profits are guaranteed as long as a firm operates ethically.