In the one-input model, profit is always maximized where marginal revenue product is equal to the input price.

Answer the following statement true (T) or false (F)

False

Rationale: This is only true if the true profit-maximizing production plan is at an "interior" solution. But, if the producer choice set is non-convex, the profit maximizing plan might involve no production (or infinite production) -- and in those cases, marginal revenue product is not equal to input price.

You might also like to view...

People who choose not to participate in fair gambles are called

a. risk takers. b. risk averse. c. risk neutral. d. broke.

The term "invisible hand" was coined by

a. Adam Smith. b. David Ricardo. c. Karl Marx. d. Benjamin Franklin.

Assume that taxes depend on income. The MPC is 0.8 and t is 0.4. If government purchases increase by $100 billion, the equilibrium level of output will increase by

A. $16.7 billion. B. $57.5 billion. C. $192.31 billion. D. $215.9 billion.

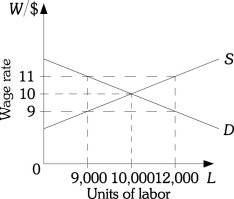

Refer to the information provided in Figure 28.2 below to answer the question(s) that follow. Figure 28.2Refer to Figure 28.2. If this firm pays the efficient wage of $9

Figure 28.2Refer to Figure 28.2. If this firm pays the efficient wage of $9

A. the supply of labor will increase until $9 is also the equilibrium wage. B. the firm's demand for labor will decrease until $9 is also the equilibrium wage. C. there will be an excess demand for labor of 3,000. D. there will be an excess supply of labor of 3,000.