Gasoline and bicycles are substitutes in consumption. Suppose we increase the federal gasoline tax to $1 per gallon

Initially, the gasoline price rises due to the tax, and the demand curve for bicycles shifts rightward because these goods are substitutes. Then, the bicycle price rises, and the demand curve for gasoline shifts rightward. Assuming the general equilibrium is achieved in both markets after these two steps, which of the following statements is NOT true? A) Partial equilibrium analysis only focuses in the first-round changes in the gasoline market (ignoring the secondary effects that arise from changes in the bicycle market).

B) Partial equilibrium analysis would predict a larger shift in the price and quantity demanded for gasoline than a general equilibrium analysis.

C) The price increase in gasoline is larger under the general equilibrium approach, but the change in the quantity of gasoline demanded is smaller than under partial equilibrium analysis.

D) All of these statements are true.

B

You might also like to view...

Which of the following would be most likely to induce Congress and the president to conduct contractionary fiscal policy? A significant

A) increase in labor productivity. B) decrease in oil prices. C) increase in inflation. D) decrease in real GDP.

A firm's profit can be calculated by subtracting its total revenue from its total costs

a. True b. False Indicate whether the statement is true or false

One of the reasons that pollution problems are as large as they are is that

A. markets let individuals and firms deplete valuable resources without charging money for doing so. B. markets are incapable of incorporating valuable resources such as air and pure water. C. governments use resources without paying for them the way that individuals and firms must. D. markets are not an efficient means to address scarcity.

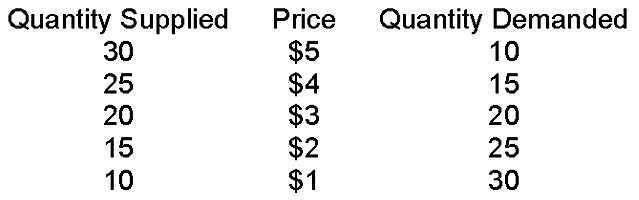

When the price is $2

A. quantity supplied is greater than quantity demanded and, therefore, price must rise to get to equilibrium.

B. quantity supplied is less than quantity demanded and, therefore, price must fall to get to equilibrium.

C. quantity demanded is greater than quantity supplied and, therefore, price must rise to get to equilibrium.

D. quantity demanded is greater than quantity supplied and, therefore, price must fall to get to equilibrium.